Recent KiwiSaver data provides an interesting snapshot of how New Zealanders are saving for the future.

Despite ongoing pressure from higher living costs, KiwiSaver balances and contributions have continued to grow, highlighting the important role the scheme plays in helping many New Zealanders build long-term financial security.

At the same time, the data also shows that contribution patterns can have a significant impact on long-term outcomes.

Contributions remain strong

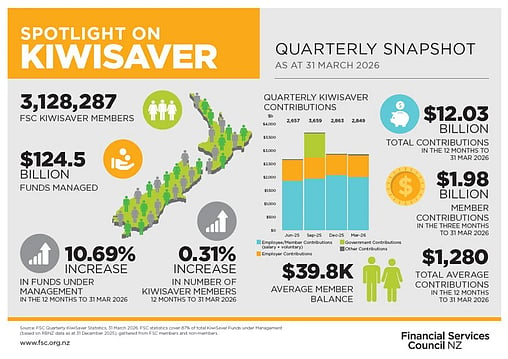

According to the latest Financial Services Council KiwiSaver Spotlight, member contributions reached $1.98 billion during the March 2026 quarter, making it the second-highest quarterly contribution total on record.

Total KiwiSaver funds under management also increased to $124.5 billion, up 10.69% over the previous 12 months.

These figures suggest that many New Zealanders continue to prioritise long-term saving, even while managing higher day-to-day expenses.

KiwiSaver balances continue to grow

Separate research commissioned by Te Ara Ahunga Ora Retirement Commission found that the average KiwiSaver balance increased to $41,286 as at the end of 2025, an increase of more than 11% from the previous year.

As KiwiSaver matures, average balances have generally increased over time, reflecting both ongoing contributions and investment growth.

The research also found that fewer members now have balances below $10,000, while a growing number have accumulated balances above $80,000.

The role of regular contributions

One of the clearest findings from the research was the difference between members who were actively contributing and those who were not.

Members who contributed during the previous 12 months had an average balance of $50,727, compared with $19,553 for non-contributing members.

While every person's circumstances are different, the data highlights how regular contributions can influence long-term savings outcomes over time.

The research also found that contribution rates were generally highest among people in their later working years, when retirement planning may become more of a focus.

Different circumstances can lead to different outcomes

The research highlighted that KiwiSaver outcomes are often influenced by factors such as income levels, employment patterns, time spent in paid work, and the ability to contribute consistently.

For example, people working part-time, moving in and out of the workforce, or experiencing contribution interruptions may build retirement savings at a slower pace than those able to contribute regularly throughout their working lives.

The report also noted that average balances differed between men and women, reflecting a range of factors including income levels and time spent outside the paid workforce.

Looking beyond short-term market movements

Investment markets often attract attention when conditions become volatile, but the latest KiwiSaver data highlights another important factor in long-term wealth building: consistency.

While market performance will always play a role, maintaining a long-term approach and contributing where possible can help support retirement savings over time.

For many New Zealanders, KiwiSaver remains one of the most significant long-term investment assets they will build during their lifetime.

If you would like to discuss your KiwiSaver plan, contribution levels, or broader retirement planning goals, please contact us.

Disclaimer: Please note that the content provided in this article is intended as an overview and as general information only. While care is taken to ensure accuracy and reliability, the information provided is subject to continuous change and may not reflect current developments or address your situation. Before making any decisions based on the information provided in this article, please use your discretion and seek independent guidance.